Attention millennials, now, listen up! It’s important to have a personal financial plan. Here is the top ten list for college-aged folks, that will help you with smart money practices and habits:

Attention millennials, now, listen up! It’s important to have a personal financial plan. Here is the top ten list for college-aged folks, that will help you with smart money practices and habits:

1 – Create a Budget – Simply stated, it’s figuring out how much money is coming in and how much money is going out. In fact, click here to download our Budget PDF. https://talkinmoney.org/files/Budget-Mania.pdf

2 – Track how much you spend – For the next seven days, track all your spending – you’ll be surprised on where the money goes!

3 – Live Within Your Means – Every first time college student will tell you how fast they blew through all their money. Don;t spend what you don;t have.

4 – Set Goals for Yourself – Take time to establish goals. Make them realistic and attainable. For example, saving towards a big purchase, or paying down your credit cards.

5 – Credit Card 101 – Speaking of paying down your credit cards, if you have the habit of paying your credit card balance fully, every month, this will go a long way in helping your credit scores!

6 – Student Loan 101 – Don’t take out college loans for anything but educational and living expenses!

7 – Never Be Late On A Payment – Always pay on time. Avoid late fees. This will tremendously help your credit score. If you are going to be late, call and talk to the company, they will always make arrangements.

8 – Create an Emergency Fund – Try to build your savings to three months living expenses.

9 – Be Smart and Save – Pinch your pennies and be smart about your spending and it will save you $$$. Here’s a resource of money-saving tips http://www.collegescholarships.org/student-living/save-money.htm

10 – Find Scholarships, Avoid Loans – There is free money for the taking in the form of scholarships. Seek those out first, before you go after that easy-to-get college loan.

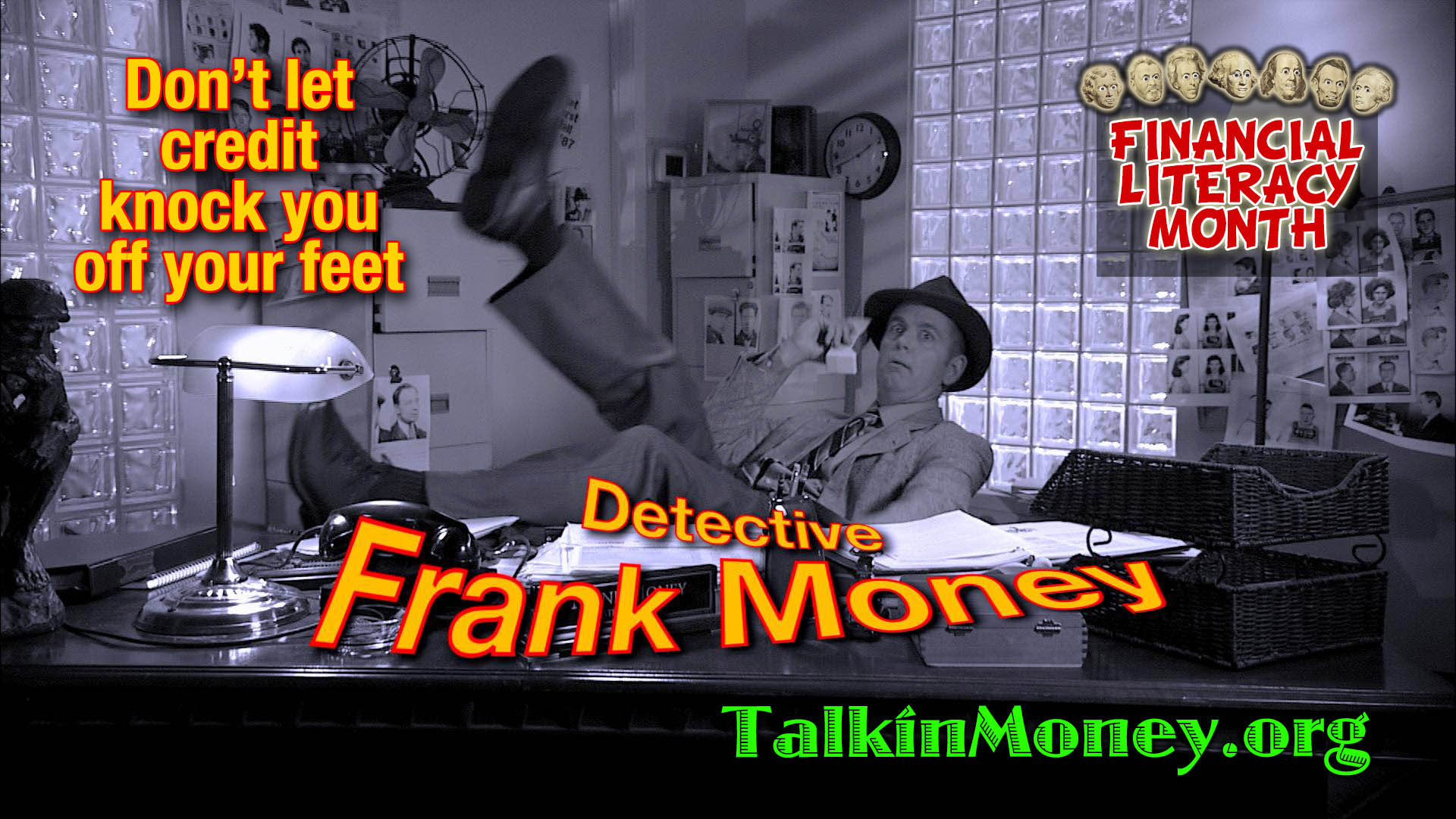

OohRah! April is National Financial Literacy Month, Talkin’ Money’s favorite month! To celebrate the importance of being financially literate, we’re going to post financial literacy tips every day.

All right all you spenders, there’s a subject near and dear to me and that’s on the subject of credit. Now you may be thinking to yourself that poor old Frank Money has no life. That may be true but I’m not poor and I’m not in debt, but thinking about the different kinds of debt can really knock me off my feet.

All right all you spenders, there’s a subject near and dear to me and that’s on the subject of credit. Now you may be thinking to yourself that poor old Frank Money has no life. That may be true but I’m not poor and I’m not in debt, but thinking about the different kinds of debt can really knock me off my feet.