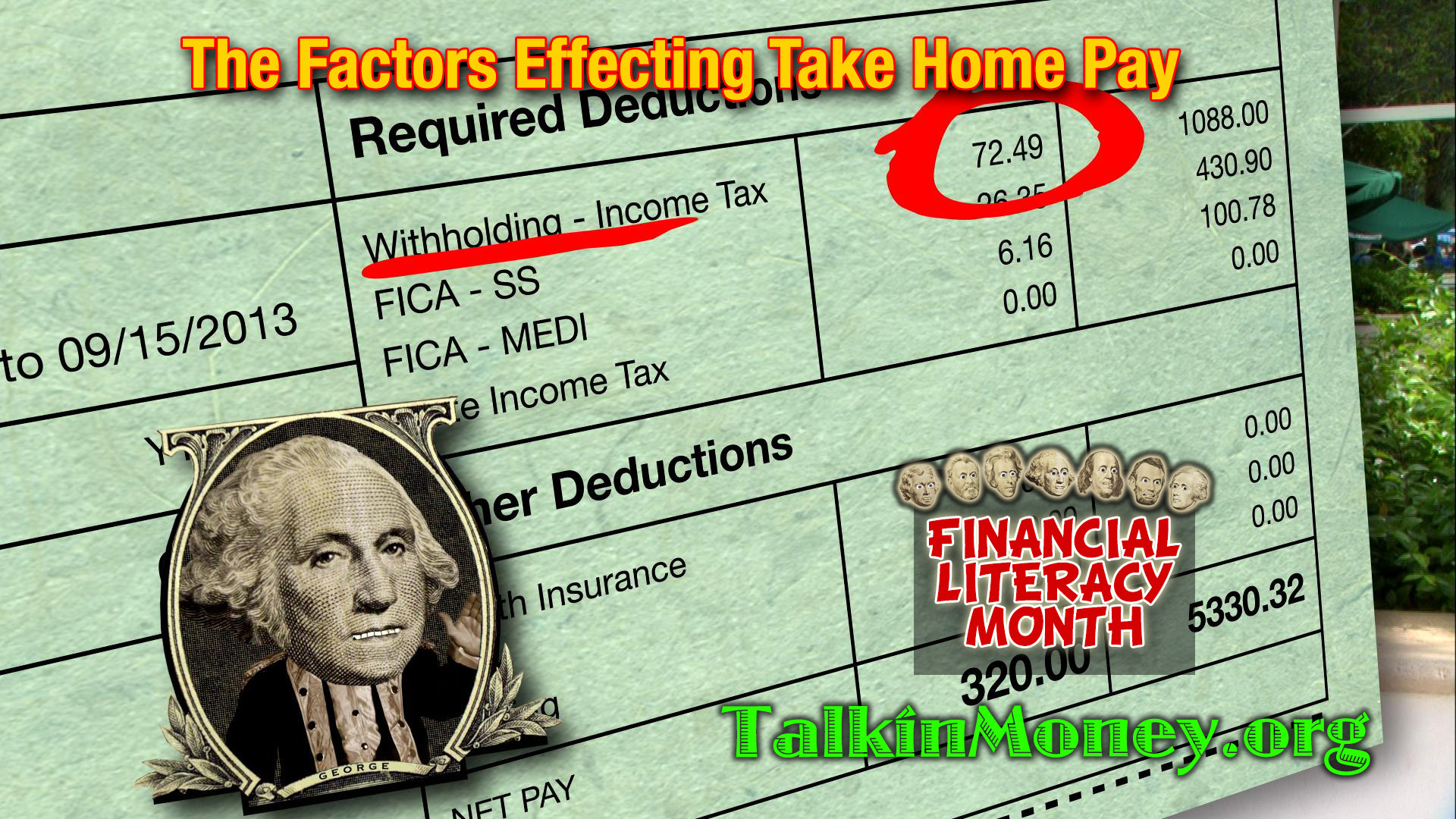

It’s just a hunch but I’m willing to bet that a lot of you earning a paycheck don’t fully understand all the deductions that are taken from your gross amount. First of all, these deductions are actually called taxes. That’s right, you’re now in that exclusive club that helps run our country as smooth as it can.

It’s just a hunch but I’m willing to bet that a lot of you earning a paycheck don’t fully understand all the deductions that are taken from your gross amount. First of all, these deductions are actually called taxes. That’s right, you’re now in that exclusive club that helps run our country as smooth as it can.

Depending on what state you live in determines how much in taxes you pay. The basic taxes we all pay are Federal Income Tax, Social Security and Medicare. Federal is just how it sounds. It pays for what’s needed throughout our country including National Defense. Social Security is there to assist you financial when you reach retirement age. Trust me, you’re going to need that. As you will with Medicare, that’s also for retirement age to assist with basic health care.

All states are not created equal when it comes to taxes. A number of states have a State Tax and could also have a City Tax. There lots of other taxes out there but I think you get the idea. Death and taxes…I’ll take taxes!

It’s Tax Day! Normally, Tax Day is April 15th, but this year it’s April 18th! Why the change to April 18th? Well, in typical Washington-DC fashion…it’s complicated…here’s the reason why –

It’s Tax Day! Normally, Tax Day is April 15th, but this year it’s April 18th! Why the change to April 18th? Well, in typical Washington-DC fashion…it’s complicated…here’s the reason why –  How many times have you passed by an electronics store and saw the X-Box you always wanted was finally on sale or the newest smart phone has hit the market? Temptations are thrown at us everyday in many different forms of ads. They know how to get your attention.

How many times have you passed by an electronics store and saw the X-Box you always wanted was finally on sale or the newest smart phone has hit the market? Temptations are thrown at us everyday in many different forms of ads. They know how to get your attention. We’ve all heard and read a thousand times how we should save on a regular basis and the younger you start the more we’ll have when getting closer to retirement. But as sure as the sun rises there will always be something that happens in your life that will make it difficult for you to part with your money to put into savings. That’s why every paycheck you should have a set portion of your salary automatically deposited into your savings account.

We’ve all heard and read a thousand times how we should save on a regular basis and the younger you start the more we’ll have when getting closer to retirement. But as sure as the sun rises there will always be something that happens in your life that will make it difficult for you to part with your money to put into savings. That’s why every paycheck you should have a set portion of your salary automatically deposited into your savings account. April 15th, ‘tax day’, always seems to be a day of chaos and dread for taxpayers – though thru some convoluted rules, ‘tax day’ is actually April 18th this year. We’ve all seen traffic jams and long lines at local Post Offices with last minute taxes held tightly in their hands hoping to get their taxes sent out on time.

April 15th, ‘tax day’, always seems to be a day of chaos and dread for taxpayers – though thru some convoluted rules, ‘tax day’ is actually April 18th this year. We’ve all seen traffic jams and long lines at local Post Offices with last minute taxes held tightly in their hands hoping to get their taxes sent out on time. When preparing for tax time don’t just assume that Federal, State and other income taxes will be the only thing you can declare hoping you’ll get some kind of tax return. Depending on what kind of job or jobs, or what kind of savings or purchases you’ve made, you may qualify to reduce your taxable income and get a larger refund.

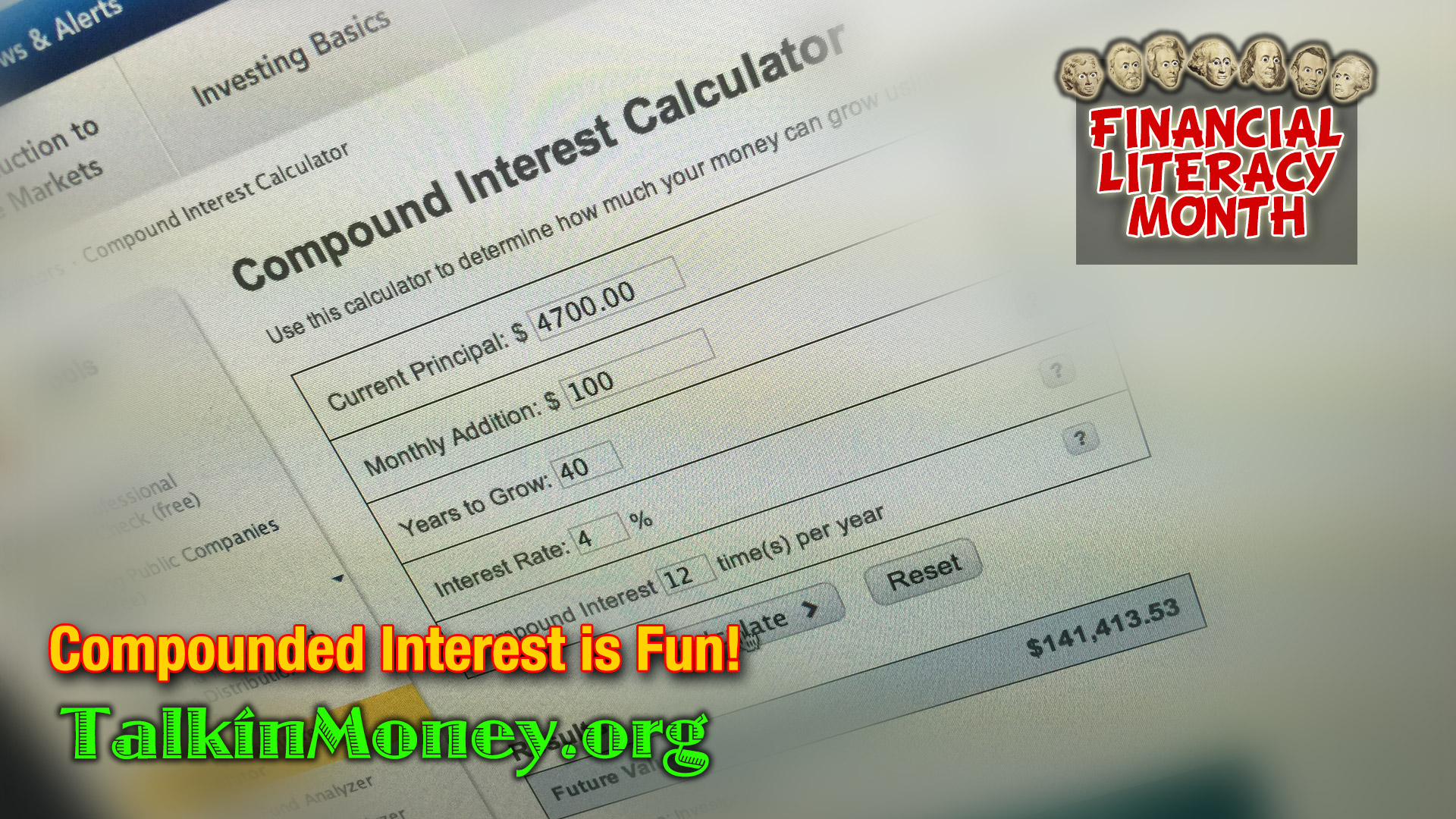

When preparing for tax time don’t just assume that Federal, State and other income taxes will be the only thing you can declare hoping you’ll get some kind of tax return. Depending on what kind of job or jobs, or what kind of savings or purchases you’ve made, you may qualify to reduce your taxable income and get a larger refund. When you’re young and just starting out in the workforce and lucky enough to be able to join in an employee sponsored savings plan but you’re not sure if you should. Here’s the answer: Yes, definitely, do not hesitate. I hope that’s clear enough. To understand it better let’s take a look at the definition.

When you’re young and just starting out in the workforce and lucky enough to be able to join in an employee sponsored savings plan but you’re not sure if you should. Here’s the answer: Yes, definitely, do not hesitate. I hope that’s clear enough. To understand it better let’s take a look at the definition. There’s one private investigator who’s middle name is ‘Identity Theft’! Talkin’ Money’s own Frank Money!

There’s one private investigator who’s middle name is ‘Identity Theft’! Talkin’ Money’s own Frank Money! When you think about it Insurance and Risk Management are really the same thing. Adults who own homes have all kinds of insurances including protecting their home and belongings. But when first starting out in the working world, or even before when attending college, insurance is also a must have.

When you think about it Insurance and Risk Management are really the same thing. Adults who own homes have all kinds of insurances including protecting their home and belongings. But when first starting out in the working world, or even before when attending college, insurance is also a must have. Here’s a question for you. What’s the most expensive purchase you’ll make in your life? A car? Nope. A house? You might think so but you would be wrong. Actually, it’s your retirement. Bet you didn’t think about that answer.

Here’s a question for you. What’s the most expensive purchase you’ll make in your life? A car? Nope. A house? You might think so but you would be wrong. Actually, it’s your retirement. Bet you didn’t think about that answer.